Disclaimer: Which dividend-paying Whole Life policy may be best for you will vary depending on your particular age, occupation, hobbies, and health situation. We are NOT one-trick-ponies. Our main value proposition is that we perform extensive analysis and anonymous shopping among the best mutual life insurance companies to find our clients the best whole life insurance policy.

All that said…

In the vast majority of situations, we are finding that Penn Mutual’s “Guaranteed® Whole Life” product is outperforming every other mutual insurance company’s dividend-paying whole life policy, with room to be wrong and still win.

Here’s why:

The base policy of Penn Mutual’s Guaranteed® Whole Life policy is one of the leanest & meanest available.

One attractive feature about Penn Mutual’s Paid Up Additions Riders is they are fully underwritten at the onset of the policy, giving you a range of flexibility and a long runway.

Many Whole Life companies have a “use it or lose it” PUA payment policy. If you don’t max-fund your policy right away or you can’t once every 3-years, you get shut out from doing future paid-up additions.

Some companies only required you to pay $100 per year into your PUA rider to keep it open. However, things happen and people forget. On my own mother’s Whole Life policy, there was confusion since the base premium was in bold. Her extra $100 wasn’t sent in that year, and just like that she lost her right to overfund for good.

With Penn Mutual’s paid-up additions rider, you only need to heavily fund it once every 5-years to keep your PUA rider fully available so you can continue to max-fund at any time during the next 5-year window. And by “heavily fund it once every 5-years”, you don’t even need to do the maximum. With Penn you only need to pay HALF of whatever your maximum PUA payment is once every 5 years to keep your option open to pay the maximum for the following 5-years.

This “half-every-5-years” flexibility window gives you time to ride out most cycles and keep your full PUA window open and available.

As with most carriers, Penn has a term rider (called the Flexible Protection Rider) that allows you to keep your Whole Life cost structure low so you can put the majority of your total premium towards paid up additions.

They offer both a level term rider and increasing term rider depending on how long you’d ideally like to over-fund your policy.

As you can see from the two graphs below, the more PUAs you pay into your policy, the quicker the term rider is replaced by purely paid up whole life insurance (which also increases your overall cash value performance as well as your cut of future dividend pools.

Keep in mind, this graphic is not displaying ultra-aggressive over-funding like we recommend. Oftentimes, our clients will completely replace their term-rider with paid-up additions by the 4th or 5th year with a max-funded infinite banking policy the way we design them.

To better understand how whole life works with the different riders for optimal performance, check out our very popular video complete with examples of optimally designed dividend paying whole life insurance.

Let’s say that during retirement you take recurring tax-exempt policy loans that you have no intention of repaying. With many other whole life policies, you have to constantly manage your loan to cash value situation and possibly even make payments throughout old age to keep your policy from lapsing.

Otherwise you may get stuck with a huge tax bill when you can afford it the least!

Penn Mutual’s Overloan Protection Rider solves that common issue when using whole life for retirement assuming the following 3 things:

- You are at least 75 years old when the policy is set to lapse from excessive loans

- Your Penn Mutual Guaranteed® Whole Life policy has been in-force for at least 15 years

- Your total policy loan equals 99% of your whole life cash value

When all 3 of these things happen, Penn Mutual’s Overloan Protection Rider will automatically freeze that remaining 1% of non-loaned cash value to preserve a minimal amount of whole life insurance for your heirs. Doing so ensures the tax-exempt status of all your prior lifetime distributions (policy loans or withdrawals) so your whole life policy stays in force preserving the tax sanctuary throughout your golden years.

Here are the benefits of this unique whole life insurance rider according to Penn Mutual:

When looking at all the other whole life companies that offer dividend-paying whole life insurance, only two companies offer this sort of protection against excessive loans when using whole life for retirement. Even then, Penn Mutual is the only company that offers it when also applying a term insurance rider in conjunction with a paid up additions rider (PUA). The other mutual holding company offers it only on their 20-pay or 10-pay whole life product, which obviously will have much less premium flexibility.

On a different note regarding loans, perhaps the only thing that someone could fault Penn Mutual with is the fact that they are a direct recognition company. This means that whatever portion of your cash value has a policy loan against it will receive either a higher or lower dividend than the portion of your cash value without a loan.

On the surface, this sounds like a bad thing, especially if you are looking for the best whole life policy for infinite banking. However, in a rising interest rate environment, direct recognition loans may be more beneficial than non-direct recognition loans.

Regardless, we often find that the superior policy performance of Penn Mutual’s Guaranteed® Whole Life usually still outperforms its best non-direct recognition peers, even when substantial loans are illustrated through the life of the policy using today’s low dividend rates.

Although most of our clients are adding whole life insurance to their financial arsenal primarily for cash value growth, private banking loans, and future tax-exempt retirement distributions, many of them overlook or underestimate this value of living benefits on a hybrid life insurance policy.

Many of the other best whole life insurance only offer living benefits or a chronic illness rider for an additional charge on their dividend paying whole life insurance policy. Penn Mutual’s Chronic Illness Accelerated Benefit Rider can be added at issue onto their Guaranteed® Whole Life policy for no additional charge and with no additional underwriting.

Essentially Penn Mutual’s Chronic Illness Benefit Access Rider can be triggered one of two ways, which happen to be very similar to the two triggers for a traditional long term care policy:

- Inability to complete at least 2 Activities of Daily Living (ADLs are bathing, dressing, eating, transferring, toileting, and continence)

- The insured has a severe cognitive impairment that requires substantial supervision by another person to protect the insured from threats to health and safety for a period of at least 90 consecutive days.

The major difference between Penn Mutual’s chronic illness rider vs. a long term care policy is the fact that these triggers can be for a temporary situation with long term care, whereas with Penn’s living benefits these triggers must be deemed to be the onset of a permanent condition according to a medical practitioner unrelated to the insured.

Also, every year you want another acceleration, the insured must be re-certified by a medical professional.

Keep in mind too that the acceleration is really just a very favorable lien against your death benefit. Here the amount of the loan is not limited by how much cash value you have as collateral because the whole life insurance companies were expecting to pay your death benefit at life expectancy.

However, these early accelerations do accrue at interest against that future receivable. That said the lien accrues at Moody’s Corporate Bond Index (4.38% as of April 10th, 2022).

At least this is a very fair and favorable present value advance, especially if you’re in bad shape, you can’t work, and really need the money.

Below is a generic example from Penn Mutual on a different product that is pure death benefit with no cash value at the time of acceleration. Remember, the exact amount you would receive during lifetime and at death is a totally dynamic figure and will depend on your age at issue, age of claim, health, death benefit, cash value, policy performance, and so on.

Keep in mind that this is an ultra-simplified example using a death benefit only product to show how Penn Mutual’s chronic illness rider allows you to accelerate the death benefit for living benefits.

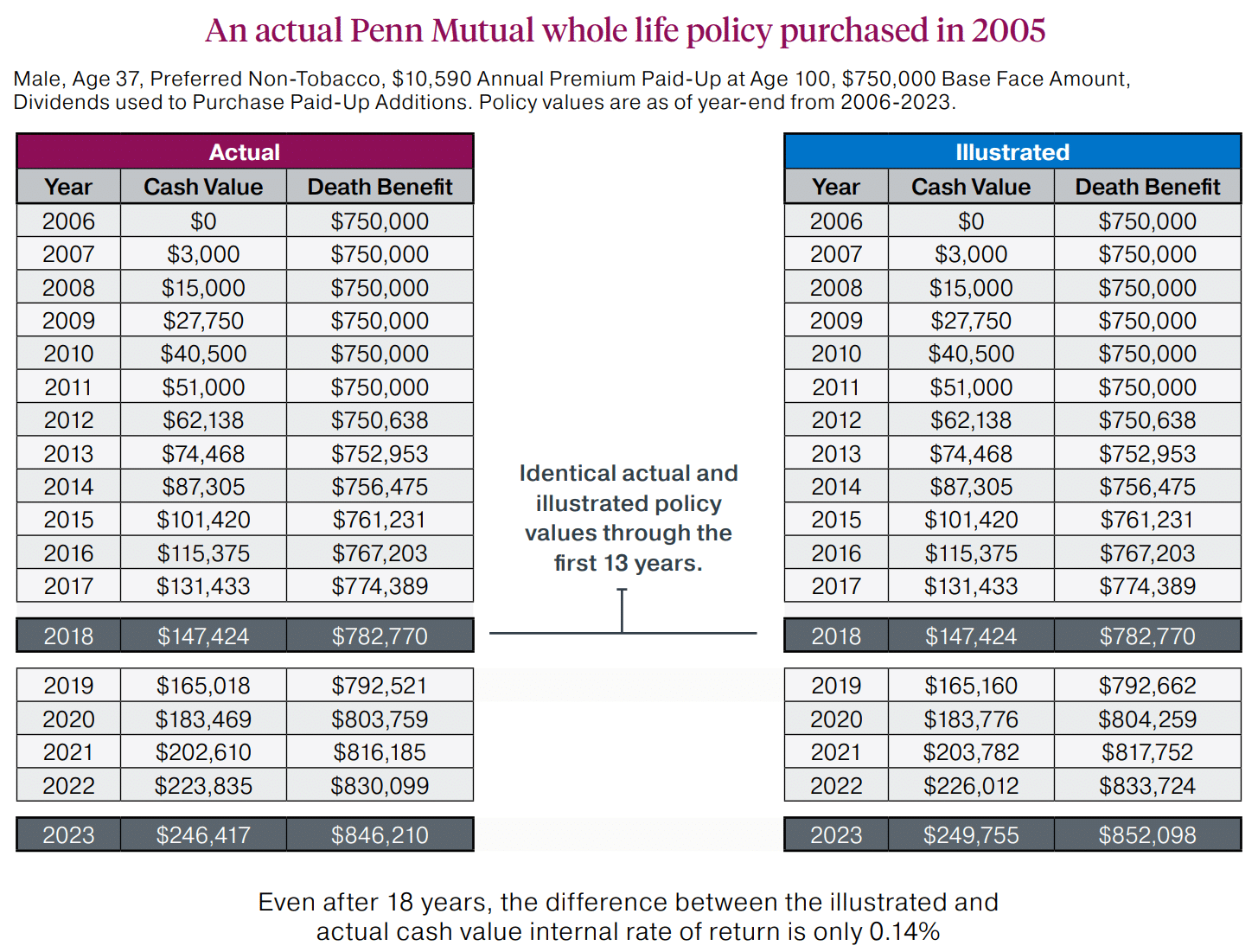

As you can see, Penn Mutual had one of the more competitive dividend histories before 2008 and without a doubt the most competitive dividend whole life policy since. Below is an example of how powerful such a consistent dividend history can be.

On the left in red shows how Penn Mutual’s actual whole life policy performed, and on the right in gray shows how it was originally illustrated 14 years prior on a whole life cash value calculator. You can see in these two whole life cash value charts that they are identical from 2006 to 2018. Only in 2019 is there a slight divergence due to a decreased dividend. Although this is a pure base policy and therefore not designed optimally for cash value, you can see the divergence widens in 2020, it is a relatively small percentage of the total cash value.